Introduction

In the world of finance, credit ratings wield immense power. They determine the ability of businesses and individuals to secure loans, access capital, and even influence investment decisions. For advisory services, mastering the credit rating game is essential to navigate the complex financial landscape effectively. This blog delves into the intricacies of credit ratings and provides invaluable insights into best practices for advisory services to optimize their clients’ creditworthiness.

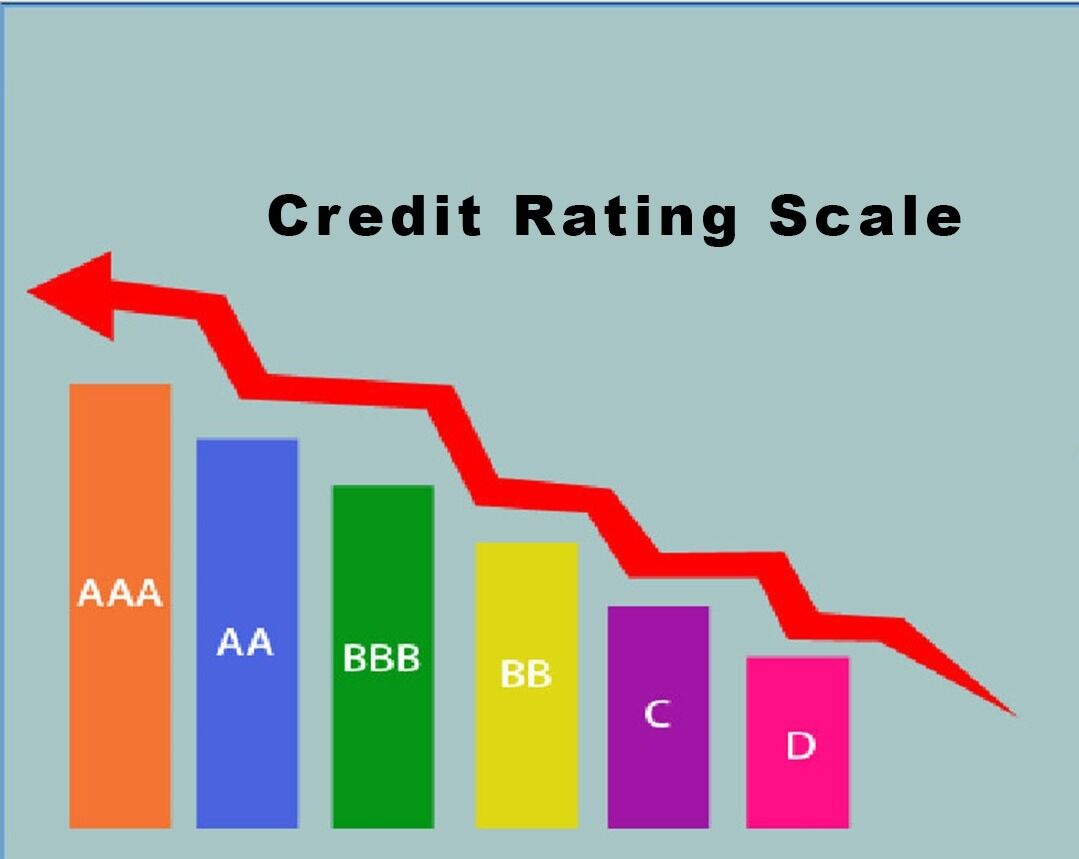

Understanding Credit Ratings

Credit ratings are assessments of a borrower’s creditworthiness, conducted by credit rating agencies CRA such as Standard & Poor’s, Moody’s, and Fitch Ratings. These ratings evaluate the likelihood of timely repayment of debt obligations based on various factors, including financial performance, industry outlook, and economic conditions. A higher credit rating signifies lower credit risk and vice versa.

Importance of Credit Ratings in Advisory Services

For businesses and individuals, credit ratings significantly impact their financial opportunities and obligations. A favorable credit rating enhances access to financing at lower interest rates, facilitates business expansion, and strengthens investor confidence. Conversely, a poor credit rating restricts access to capital, increases borrowing costs, and hampers growth prospects. In advisory services, adeptly managing and optimizing credit ratings is paramount to securing favorable financial outcomes for clients.

.